In the wake of rising costs, EV firms must allocate capital to those activities that will bolster their competitve advantage.

Electric vehicle (EV) firms should retain activities that are critical to maintaining long-term competitive advantage, and outsource those that are not, despite often painful short-term tradeoffs. The capital-intensive nature of EV manufacturing, magnified by rising capital and input costs, requires capital discipline closely aligned to the firm’s overall business strategy.

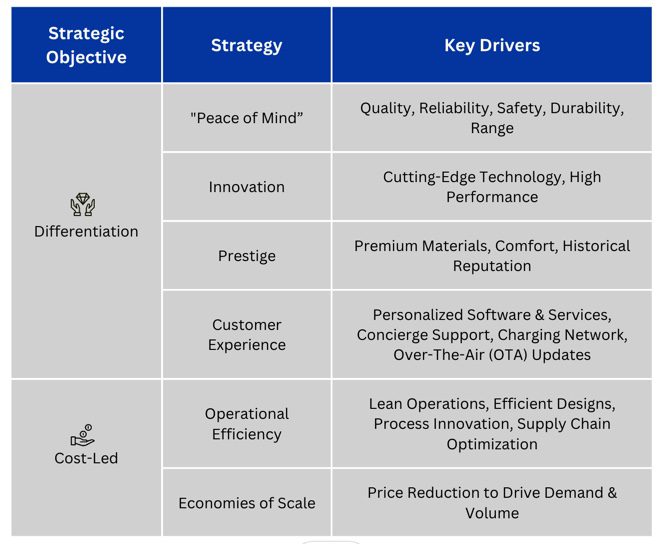

Competitive advantage in the EV industry

EV firms compete by differentiating their vehicles, leading with lower cost vehicles, or a hybrid of both. Differentiation and cost leadership can be achieved through several strategies (see figure below).

The success of a differentiation or cost-led strategy is measured by the level of profit the EV firm can extract from the price, by how long the firm can maintain that profit level, and to what extent that profit level generates returns on capital beyond the cost of capital– ie. long-term value creation. The ability to maintain a given profit level is heavily influenced by competitor offerings from which customers can select. To enhance their ability to stand out from the competition, firms should align their value chain to their chosen strategy.

Value chain as driver of competitive advantage

Armed with clarity on their competitive strategy, EV firms should evaluate each value chain activity on its importance in maintaining competitive advantage, and its ability to create long-term value for the firm. An initial evaluation can be performed by asking this question for each activity: “Given our selected strategy, will retaining this activity allow us to maintain higher prices or lower costs in the long run relative to an outsourced alternative?”

importance in maintaining competitive advantage, and its ability to create long-term value for the firm. An initial evaluation can be performed by asking this question for each activity: “Given our selected strategy, will retaining this activity allow us to maintain higher prices or lower costs in the long run relative to an outsourced alternative?”

By basing vertical integration and outsourcing decisions on long-term competitive strategy, rather than short-term cost or operational pressures, EV firms can improve the likelihood of success in an increasingly competitive market. Investors can also use the below approach to prioritise portfolio allocation and avoid firms without a clearly articulated strategy for long-term value creation.

Applications in practice

Depending on the overall competitive strategy of the firm, the answer to the above question will be different for each activity in the value chain. For instance, a differentiation strategy based on an exceptional customer experience may suggest retaining all software related activities as well as sales and service, while outsourcing manufacturing, logistics, component manufacture and even elements of hardware development.

A cost led strategy based on operational efficiency may suggest the near opposite: owning hardware development, manufacturing, and logistics, while licensing third party software and using a traditional dealer network for sales and service. Component make vs buy decisions can be made on a case-by-case basis. A firm with a differentiation strategy based on innovation and prestige may be tempted to bring component manufacturing in-house from a struggling supplier, but then decide owning manufacture of a low margin commodity is not an efficient use of capital in the long-term. Despite the short-term cost, they may decide to retool with another supplier or develop the current one.

Real-world complexities

Value chain activities are not modular. Many have interdependencies to be managed and real-world competitive pressures may cause firms to deviate from the suggestions implied by the above model. For instance, there are additional business-critical support functions that enable synergies between value chain activities. A strong purchasing function can drive incremental value by fostering collaboration between hardware development teams, raw material and component suppliers, and manufacturing plants. A firm may decide to keep many of these activities in house to realise the full benefit of these synergies.

Risk mitigation is another consideration. Demand for battery cells and required raw materials is expected to outstrip supply over the next decade. To secure supply and de-risk the business, a firm may decide to invest in battery component and material capacity.

Short-term survival may take precedence in certain instances. Some firms may outsource manufacturing as the only viable path to market before exhausting their funding runway, even if it conflicts with their long-term strategy. In those cases, the firm should carefully consider investing in other activities in the value chain, such as software, that will give them a durable competitive advantage.

Strategic discipline

With rising capital and material input costs, EV firms should stay laser-focused on how they intend to maintain competitive advantage in the long-term, and allocate capital to those activities that will bolster that advantage. This is especially true when evaluating opportunities that may provide a short-term benefit, although could drag on performance over time.

About the authors: Ryan Simerlink is a Strategy Consultant with Accenture addressing Procurement activities in the Automotive and Technology sectors. Adam Robbins is a Strategy Consultant with Accenture focused on Automotive, Industrial and Supply Chain matters. Adam Regier is a Consultant with Accenture focused on Automotive and Direct Materials strategic advisory. Ryan Stover is a Consultant with Accenture focused on Automotive and Industrial Manufacturing topics